With COVID travel restrictions now a thing of the past, it’s time for an annual refresher on the best cards for overseas spending.

While it’s “free” to use your credit card in Singapore (unless the merchant imposes a surcharge- which they shouldn’t!), swiping it overseas entails an explicit cost due to foreign currency (FCY) transaction fees imposed by banks.

And yet, many credit cards offer an upsized rate on FCY transactions. For example:

- UOB PRVI Miles Cardholders earn 1.4 mpd for all SGD spending, but 2.4 mpd for FCY spending

- DBS Altitude Cardholders earn 1.2 mpd for all SGD spending, but 2.0 mpd for FCY spending

So the question therefore is whether it’s worth using your card overseas, and the answer depends on:

- How much you value a mile

- How much you’re paying for miles when you use your card overseas

(1) is a subjective measure, which I’ve addressed in this article (my personal value is about 1.5 cents). (2) is much more objective, and the focus of the discussion below.

How much do banks charge for foreign currency transactions?

When you make a credit card transaction in a currency other than Singapore Dollars, what typically happens is the amount is first converted to USD, and then into SGD (based on rates provided by Mastercard or Visa).

| 💳 Example: DBS Bank |

| “Visa/Mastercard transactions in US Dollar shall be converted to Singapore Dollar on the date of conversion. Transactions in other foreign currencies will be converted to US Dollar before being converted to Singapore Dollar.” |

There’s some spread involved here (usually <0.5%), but the biggest expense is the FCY transaction fee charged by the bank. Here’s a summary:

| 💳 FCY Fees by Issuer and Card Network | ||

| Issuer | ↓ Visa & Mastercard | AMEX |

| Standard Chartered | 3.5% | N/A |

| Citibank | 3.25% | 3.3% |

| DBS | 3.25% | 3% |

| HSBC | 3.25% | N/A |

| Maybank | 3.25% | N/A |

| OCBC | 3.25% | N/A |

| UOB | 3.25% | 3.25% |

| BOC | 3% | N/A |

| CIMB | 3% | N/A |

| American Express | N/A | 2.95% |

FCY fees range from 2.95% to 3.5%, and unfortunately, have been edging ever upwards over the years.

- On 1 Apr 18, Maybank increased its FCY charge on Visa Diamante, Visa Infinite and World Mastercard from 2.5% to 2.75%

- On 4 Oct 18, Citibank increased its FCY charge from 2.8% to 3%

- On 1 Nov 18, HSBC increased its FCY charge from 2.5% to 2.8%

- On 1 Jan 19, CIMB removed the admin fee waiver for FCY transactions on the Visa Signature and Platinum Mastercard, effectively increasing the fee from 1% to 3%

- On 2 Jan 19, DBS increased its FCY charge from 2.8% to 3%

- On 15 Jan 19, BOC increased its FCY charge on Mastercard transactions from 2.5% to 3% (Visa fees increased from 2.5% to 3% on 1 Dec 18)

- On 15 Mar 19, OCBC increased its FCY charge from 2.8% to 3%

- On 4 Sep 19, UOB increased its FCY charge from 2.8% to 3.1%

- On 1 Nov 19, DBS increased its FCY charge from 3% to 3.25%

- On 3 Dec 19, OCBC increased its FCY charge from 3% to 3.25%

- On 15 Dec 19, Citibank increased its FCY charge from 3% to 3.25%

- On 1 Mar 20, AMEX increased its FCY charge from 2.5% to 2.95%

- On 9 Mar 20, UOB increased its FCY charge from 3.1% to 3.25%

- On 1 Nov 21, Maybank increased its FCY charge from 2.75% to 3.25%

- On 4 Jan 23, HSBC increased its FCY charge from 2.8% to 3.25%

Don’t forget that the FCY fees are charged on top of the implicit spread in the Mastercard or Visa exchange rate. For example:

- A US$100 transaction charged to a Mastercard would cost S$134.81, assuming no FCY fees (spot rate: S$134.12)

- Once a 3.25% FCY fee is factored in, that amount becomes S$139.19

| ❓ How much will my overseas transaction cost? |

| If you’re curious as to how much a given foreign currency transaction will cost, you can use the Mastercard or Visa currency converter calculators. All you need to plug-in is the bank’s FCY fee, from the table above. |

| Mastercard Calculator |

| Visa Calculator |

What’s the cost per mile?

No one likes to pay more than they have to, but do the miles earned for overseas transactions justify the costs? Generally speaking: yes, although some cards represent better options than others.

General Overseas Spending

The following cards offer bonuses on all foreign currency transactions (except those in the general exclusions list like charitable donations and cryptocurrency).

| Card | FCY Earn Rate | Fee* | CPM |

UOB Visa Signature UOB Visa Signature | 4.01 | 3.25% | 0.81 |

SCB VI SCB VI | 3.02 | 3.5% | 1.17 |

SCB Rewards+ SCB Rewards+ | 2.93 | 3.5% | 1.21 |

DBS Treasures Black Elite DBS Treasures Black Elite | 2.4 | 3.25% | 1.35 |

UOB PRVI Miles UOB PRVI Miles | 2.4 | 3.25% | 1.35 |

OCBC VOYAGE (Premier, PPC, BOS) OCBC VOYAGE (Premier, PPC, BOS) | 2.3 | 3.25% | 1.41 |

HSBC VI HSBC VI | 2.254 | 3.25% | 1.44 |

OCBC Premier VI OCBC Premier VI | 2.24 | 3.25% | 1.45 |

| 2.2 | 3.25% | 1.48 | |

OCBC VOYAGE OCBC VOYAGE | 2.2 | 3.25% | 1.48 |

AMEX KrisFlyer Ascend AMEX KrisFlyer Ascend | 2.05 | 2.95% | 1.48 |

AMEX KrisFlyer Credit Card AMEX KrisFlyer Credit Card | 2.05 | 2.95% | 1.48 |

OCBC 90°N Card OCBC 90°N Card | 2.1 | 3.25% | 1.55 |

DBS Altitude Visa DBS Altitude Visa | 2.0 | 3.25% | 1.63 |

| 2.0 | 3.25% | 1.63 | |

Citi Prestige Citi Prestige | 2.0 | 3.25% | 1.63 |

UOB VI Metal UOB VI Metal | 2.0 | 3.25% | 1.63 |

SCB X Card SCB X Card | 2.0 | 3.5% | 1.75 |

| *Fee refers to the FCY transaction fee imposed by banks, and does not include the spread charged by Mastercard or Visa, which can add an additional 0.3-0.5% depending on currency 1. Min. spend S$1,000 per statement month, cap at S$2,000 per statement month 2. Min. spend S$2,000 per statement month, otherwise 1 mpd 3. Cap at S$2,222 per membership year 4. Min. spend S$50,000 in previous membership year, otherwise 2 mpd 5. Only in June and December, otherwise 1.1 (Blue) or 1.2 (Ascend) | |||

Specific Overseas Spending

If you’re clocking FCY spend on particular categories, the cards below can also be options.

| Card | Earn Rate | Fee* | CPM |

UOB Lady’s Card UOB Lady’s Card | 6.01 | 3.25% | 0.54 |

UOB Lady’s Solitaire Card UOB Lady’s Solitaire Card | 6.02 | 3.25% | 0.54 |

| 4.03 | 3.25% | 0.81 | |

| 4.04 | 3.25% | 0.81 | |

OCBC Titanium Rewards OCBC Titanium Rewards | 4.05 | 3.25% | 0.81 |

UOB Pref. Plat. Visa UOB Pref. Plat. Visa | 4.06 | 3.25% | 0.81 |

HSBC Revolution HSBC Revolution | 4.07 | 3.25% | 0.81 |

| *Fee refers to the FCY transaction fee imposed by banks, and does not include the spread charged by Mastercard or Visa, which can add an additional 0.3-0.5% depending on currency 1. Pick 1: Beauty & wellness, dining, entertainment, family, fashion, transport, travel (T&Cs) 2. Pick 2: Beauty & wellness, dining, entertainment, family, fashion, transport, travel (T&Cs) 3. Department store, apparel, or online transactions (excluding travel). First S$1K per statement month (T&Cs) 4. Online transactions. First S$2K per calendar month (T&Cs) 5. Department stores, apparel, electronics. First S$13,335 per membership year (T&Cs) 6. Apparel, electronics, dining, food delivery, entertainment. Also applies to overseas mobile payments. First S$1.1K per calendar month (T&Cs) 7. Airlines, hotels, department stores, apparel, supermarkets, transport. Must be online or via contactless payments. First S$1K per calendar month (T&Cs) | |||

The big news this year is obviously the UOB Lady’s Cards’ upsized 6 mpd earn rate, that runs from now till 29 February 2024.

UOB Lady’s Cardholders will earn 6 mpd on the first S$1,000 per month spent on their choice of one bonus category, whether in SGD or FCY. UOB Lady’s Solitaire Cardholders will earn 6 mpd on the first S$3,000 per month spent on their choice of two bonus categories, whether in SGD or FCY.

Bonus categories include beauty & wellness, dining, entertainment, family, fashion, transport and travel. These can be rotated every calendar quarter, if you wish.

| Category | MCCs | Description |

| (1) Beauty & Wellness | 5912, 5977, 7230, 7231, 7298, 7297 | Discount, Mass and Drug Stores, Cosmetics Stores, Barber and Beauty Shops, Health and Beauty Spa, Massage Parlours |

| (2) Dining | 5811, 5812, 5814, 5499 | Caterers, Eating places and Restaurants, Fast food restaurants and food deliveries |

| (3) Entertainment | 5813, 7832, 7922 | Bars, Taverns, Lounges and Nightclubs, Motion Picture Theatres, Theatrical Producers and Ticket Agencies |

| (4) Family | 5411, 5641 | Grocery stores, Children and Infants wear store |

| (5) Fashion | 5311, 5611, 5621, 5631, 5651, 5655, 5661, 5691, 5699, 5948 | Department Stores, Men’s and Boy’s Clothing and Accessories Store, Women’s Ready-to-wear Stores, Women’s Access and Specialty, Family Clothing Stores, Sports and Riding Apparel Stores, Shoes Stores, Men’s and Women’s Clothing Stores, Miscellaneous Apparel and Accessories Shops, Luggage and Leather Stores |

| (6) Transport | 4111, 4121, 4789, 5541, 5542 | Local Commuter Transport, Taxi, Cabs, Limousines and Travel Service, Service Stations and Automatic Gas Dispensers |

| (7) Travel | Refer to this post for the full list of eligible merchants | |

Unfortunately, the UOB Lady’s Card is limited to females only. If you lack the right equipment, then your next best alternative may be to pair a Citi Rewards Card to Amaze (see below) and use that instead, or else use the UOB Preferred Platinum Visa or UOB Visa Signature.

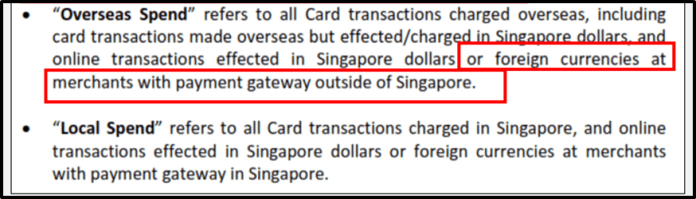

How do banks define overseas transactions?

For most banks, an “overseas transaction” is simply any transaction processed in a currency other than Singapore dollars.

But Bank of China and UOB add another caveat: the transaction must be processed outside of Singapore. For example, if you were to book through the Hotels.com Singapore website and pay in Euros with your UOB PRVI Miles Card, you’d earn 1.4 mpd instead of 2.4 mpd because the payment is processed in Singapore.

How do you know where payments are processed? You don’t. That’s the worst thing about such a rule: it puts the onus on the customer to find out information that’s not readily available.

If it’s any consolation, this is only an issue for online transactions. If you’re physically overseas when using your card, you don’t need to worry about where the payment gateway is located.

The Amaze Alternative

Despite its recent nerfs, Amaze is still one of the best options to use for overseas transactions.

With Amaze, you’ll pay an implicit FCY fee of about 1.5% while earning up to 6 mpd on your credit card plus InstaPoints (which can be redeemed for cashback). This makes it a far superior option to any traditional credit card.

|

| Apply here |

| Use code 7HK2A2 for 225 bonus InstaPoints |

| 💳 tl;dr: Amaze Card |

|

The miles earned are limited only by the credit card linked to the Amaze, and I’d recommend the following:

| 💳 Amaze Pairings | ||

| Card | Earn Rate | Cap |

UOB Lady’s Card UOB Lady’s Card | 6 mpd1 | S$1K per c. month |

UOB Lady’s Solitaire UOB Lady’s Solitaire | 6 mpd2 | S$3K per c. month |

| 4 mpd3 | S$1K per s. month | |

OCBC Titanium Rewards OCBC Titanium Rewards | 4 mpd4 | S$13.3K per m. year |

KrisFlyer UOB Credit Card KrisFlyer UOB Credit Card | 3 mpd5 | None |

UOB PRVI Miles MC UOB PRVI Miles MC | 1.4 mpd | None |

| 1.3 mpd | None | |

OCBC 90°N MC OCBC 90°N MC | 1.3 mpd | None |

| 1.2 mpd | None | |

| 1. Pick 1: Beauty & wellness, dining, entertainment, family, fashion, transport, travel (T&Cs) 2. Pick 2: Beauty & wellness, dining, entertainment, family, fashion, transport, travel (T&Cs) 3. All transactions except travel (airlines, hotels, rental cars, tour agency, cruises etc.) (T&Cs) 4. Electronics, clothes, bags, shoes and shopping (T&Cs) 5. Dining, shopping, travel, transport. Must spend at least S$800 on SIA Group transactions in a membership year (T&Cs) | ||

A brief reminder of the ground rules for Amaze:

- All Amaze transactions code as online

- All Amaze transactions will be billed in SGD

- All Amaze transactions retain the original MCC of the underlying transaction

- Amaze can be paired with any Mastercard credit or debit card

- You can save a maximum of five cards to Amaze

- DBS/POSB cards no longer award points for Amaze transactions

This rules out pairing the DBS Woman’s World Card, or some otherwise excellent options like the HSBC Revolution or UOB Preferred Platinum Visa.

Beware of DCC!

Here’s my customary warning about the scam known as Dynamic Currency Conversion (DCC).

For the uninitiated, DCC is a “service” provided by merchants which converts the transaction into your card’s local currency, at a fee that’s much more than what your bank would charge. The merchant pockets part of the profit, so some unscrupulous places will instruct staff to select it by default, without the consent of the customer.

Be alert, and always, always emphasise that you want to be billed in whatever the local currency is. If you want to avoid the scourge of DCC altogether, use an American Express card, since AMEX does not support DCC.

Conclusion

Does it make sense to use your credit card overseas? I’d say yes, assuming you can earn 4/6 mpd on the transaction. This means focusing on specialised spending cards like the UOB Visa Signature, or the Amaze + UOB Lady’s Card/Citi Rewards Card combo.

Of course, if you don’t value miles at all then you’re better off looking at a Revolut or YouTrip type solution, since these offer superior exchange rates at the expense of earning rewards.

Does DBS WMC still give 4mpd when paired with Amaze? Some of the comments seem to suggest otherwise.

As of last month’s points crediting (transactions from Sep’21), I got my 4 mpd with DBS WWMC on 15th Oct for all my Amaze transactions, except the ones made on CardUp using my Amaze card.

Should HSBC revo be added to the list given it offers 4mpd albeit not on all categories and only 2.8% FCY fee? But most of what a general person would spend overseas would be on the categories that HSBC whitelists anyway e.g. airline, hotel, car rental, dining, travel agencies, supermarket, department stores, even uber (transport)?

revo is there, under specialised spending cards.

Thanks! Must have missed it. Think it’s the most attractive one for me given the low cpm

Thanks to your kind introduction of the Amaze card. It is now my default card for overseas expenditures.

How about pairing OCBC Titanium Rewards with Amaze? It does earn 4 mpd for shopping?

following. but my understanding from the other article seems to suggest so.

I’d also like to know if i charge foreign currency through amaze to ocbc 90n mc, is it considered foreign currency or sgd? because 90n gives 1.2mpd for local spend but 2.1mpd for forex, so it might actually be worth it to charge as forex despite the 3.25% fcy.

Does Amex Krisflyer card only earn 2MPD during the months of Jun and Dec?

correct

Hi Aaron, is the CPM for the American Express Platinum Charge Card also 0.98 cpm? Thanks!

What if a merchant charges DCC without giving me a choice (aka press yes and print for me to sign). what can I do?

Check before signing and ask them to reverse then charge in local currency.

What if they “refuse”?

Dispute. No DCC gives only the SGD value for you to sign. It’s either FCY (in which case you can dispute) or FCY and SGD with boxes (in which case you tick the FCY box). Without a signature indicating your agreement, your bank will not honour thew charge. Had this several times with an StR…

https://milelion.com/2018/11/19/how-i-fought-and-won-a-dcc-dispute/

Hi Aaron, should Amaze cashback be reflected as 0.5% in the conclusion?

It’s 1% for overseas spend

I just came back from a 10-day trip and had been using Visa paywave (Apple Pay or the credit card directly). I was quite surprised that I wasn’t hit by DCC at all. All transactions were processed in the local currency without me even asking. Not sure if it was because DCC was not supported by contactless payments, or DCC was banned in that country?

Thanks for the review! I used the Amaze card with DBS WWMC for my entire UK trip! I won’t be applying for the CitiRewards card though, as I have too many cards. Pity that from 1 June, DBS WWMC will no longer be useful when tagged to the Amaze card for miles. I would be using ICBC Global travel mastercard instead (though this one no miles but has 3% cashback on overseas spend).

May I know why the Amex CPM is 0.98 for the krisflyer cards? it looks like it should be 2.95/2 = 1.475?

thanks for spotting that. have fixed it.

Sorry new to all this. For hsbc revolution, if I were to use pay wave overseas at a restaurant, will it be counted as 4mpd? Does this work by categories regardless if local or overseas? Sorry for the many questions. Thanks

Yes, overseas is fine

Hi Aaron, it’s probably time for an Amaze update. I find I’m getting charged ~2% spread for FCY transactions. Tested in TH, TW, MY in the last 2 months

Writing something on this, thanks!

Which card should I use for big ticket (5-figure) overseas spending? I noticed that all the cards mentioned above have a 1-2k monthly limit, except maybe for OCBC Titanium Rewards with a S$13,335 limit for the first year.

good point. Im asking the same too especially 1 branded bag already cost 30K

Just calculate the theoretical average mpd on your big ticket purchase and measure it against using a general spending card with no cap?

Hey guys, anyone has any tips to spend $800 on reasonable items on KrisShop to hit the SIA Group Spend? Thank you!

Having just made a big fuss with Amazon JP on the constant auto-DCC, I was surprised that my side by side purchases ended up cheaper on the Amazon DCC, though when taking the Amaze cashback into account, Amaze still beat out Amazon by a whisker. So so will continue to manually switch to local currency, but at least Amazon seems to offer a much more reasonable conversion now.

Amex converts to USD before converting to SGD. So on paper it is 2.95%, but you get hit with their FX spread twice, which usually leads to a worse outcome than any card with a 3.25-3.5% headline charge

Don’t all cards convert to USD before sgd?

UOB converts non-USD, non-AUD and non-SGD to USD before converting to SGD. So AUD and USD are the exception that gets converted to SGD directly. See https://www.uob.com.sg/personal/cards/credit-cards/terms-and-conditions.page

maybe I should rephrase, with other cards you pay the masterard/visa spread which is typically around 0.5% above mid-market. with amex you just get a really poor fx outcome, which is sad, since they control the entire chain. so lowest fee, but also poorest (typically) fx rate.

most of the times i have tracked, i have always received poorest SGD outcome with amex. so based on personal datapoints, i only use my amex when the final SGD figure is not my main concern

Does HSBC Evo give 4mpd for contactless overseas dining?

Citi Premiermiles is also running a 4mpd for till end June!