In June 2022, DBS finally decided to join the $120K party with the DBS Vantage Card, its metal offering for the mass affluent segment.

At launch, it offered a beefy 80,000 miles sign-up offer, plus 4 mpd on dining and petrol. Together with perks like an Accor Plus Explorer membership and 10 lounge visits, it was a very compelling offer for the first year.

But the honeymoon’s now over. The 4 mpd bonuses are no more, and while DBS has periodically brought back its 80,000 miles sign-up offer (with a reduced minimum spend), that’s a first-year-only perk. With the $120K segment more competitive than ever, is there a case to be made for renewal?

DBS Vantage Card DBS Vantage Card | |

| 🦁 MileLion Verdict | |

| ☐ Take It ☑ Take It Or Leave It ☐ Leave It | |

| Wit no more bonuses on petrol and dining, the DBS Vantage Card is a more marginal proposition. The math can still work, but you’ll need to work harder. | |

| 👍 The good | 👎 The bad |

|

|

| Full List of Credit Card Reviews | |

Overview: DBS Vantage Card

Let’s start this review by looking at the key features of the DBS Vantage Card

| |||

| Apply | |||

| Income Req. | S$120,000 p.a. | Points Validity | 3 years |

| Annual Fee | S$594 | Min. Transfer | 5,000 DBS Points (10,000 miles) |

| Miles with Annual Fee | 25,000 | Transfer Partners |

|

| FCY Fee | 3.25% | Transfer Fee | S$27 |

| Local Earn | 1.5 mpd | Points Pool? | Yes |

| FCY Earn | 2.2 mpd | Lounge Access? | Yes: 10x Priority Pass |

| Special Earn | 6 mpd on Expedia | Airport Limo? | No |

| Cardholder Terms and Conditions | |||

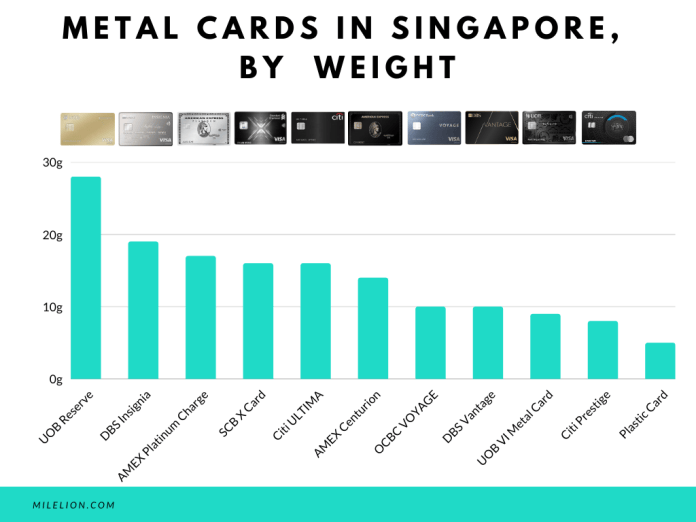

The DBS Vantage comes in metal cardstock, and weighs in at 10g. That makes it one of the lighter metal cards on the market, if that sort of thing is important to you.

The card is Paywave-equipped, and can also be added to Apple, Google or Samsung Pay.

How much must I earn to qualify for a DBS Vantage Card?

The DBS Vantage Card has a S$120,000 p.a. income requirement, and for the moment, it looks like DBS is applying this very strictly.

How strict? For starters, you won’t even be able to see the DBS Vantage Card on the DBS/POSB ibanking card application portal if your income records with DBS reflect earnings of less than S$120,000. In fact, this caused a lot of confusion during the launch week, so much so that DBS set up a dedicated landing page to address it.

You will need to update your income records with DBS before you can apply for the DBS Vantage Card. DBS/POSB customers can visit this link to update their income, which will take five working days to process.

Therefore, if you haven’t hit the magic S$120,000 figure yet, I wouldn’t be too optimistic about getting approved.

Sign-up Bonus

New DBS Vantage Cardholders who apply by 30 June 2023, spend S$4,000 within 30 days of approval and pay the first year’s S$594 annual fee will receive the following:

| Miles | |

| Pay S$594 annual fee | 25,000 miles |

| Spend S$4,000 within 30 days | 35,000 miles |

| Total | 60,000 miles |

| Must apply with promo code VANMILES | |

| ❓ “New” Definition | |

| New cardmembers are defined as customers who are currently not holding on to any principal DBS/POSB Credit Card and have not cancelled any principal DBS/POSB Credit Card within the last 12 months. | |

This bonus is on top of whatever base miles you normally earn with the DBS Vantage, so you’re looking at at least 66,000 miles in total (S$4,000 @ 1.5 mpd).

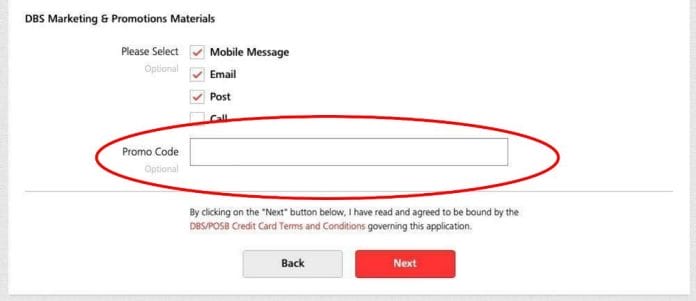

You must enter the promo code VANMILES when applying. The promo code field can be found towards the bottom of the application page, under the “DBS Marketing & Promotions Materials” section.

The 25,000 miles for paying the S$594 annual fee will be awarded immediately (in the form of 12,500 DBS points) when the annual fee is charged.

The 35,000 miles for the sign-up bonus will be credited within 90-120 days from the date of fulfilling the qualifying spend (in the form of 17,500 DBS points).

How much is the DBS Vantage Card’s annual fee?

| Principal Card | Supp. Card | |

| First Year | S$594 | Free |

| Subsequent | S$594 | Free |

The DBS Vantage Card has an annual fee of S$594 for the principal cardholder, and no fee for supplementary cards.

The first year’s fee must be paid. Subsequent years’ fees can be waived if cardholders spend at least S$60,000 per membership year.

Paying the annual fee gets you 25,000 miles in return, which means buying miles at ~2.35 cents each. While that sounds much higher than what a mile should be worth, you need to factor in the other card benefits too.

| ❓ What do I get if I qualify for a waiver? |

| If you qualify for a subsequent year fee waiver, you will not receive the 25,000 miles. However, you will still receive all the other benefits, including a renewal of Accor Plus membership and 10 more lounge visits. |

How many miles do I earn?

| 🇸🇬 SGD Spending | 🌎 FCY Spending | ➕ Bonus Spending |

| 1.5 mpd | 2.2 mpd | 6 mpd on Expedia |

SGD/FCY Spending

DBS Vantage Card cardholders earn 3.75 DBS Points for every S$5 spent in Singapore Dollars, and 5.5 DBS Points for every S$5 spent in foreign currency(FCY).

1 DBS point is worth 2 miles, so that’s an equivalent earn rate of 1.5 mpd for local spending, and 2.2 mpd for FCY spending.

This makes the DBS Vantage among the highest-earning cards in the $120K segment; the highest, if you consider the fact it has no minimum spend requirement.

| Card | SGD | FCY |

SCB VI SCB VI | Up to 1.4 mpd* | Up to 3 mpd* |

DBS Vantage DBS Vantage | 1.5 mpd | 2.2 mpd |

OCBC VOYAGE OCBC VOYAGE | 1.3 mpd | 2.2 mpd |

HSBC VI HSBC VI | Up to 1.25 mpd^ | Up to 2.25 mpd^ |

UOB VI Metal Card UOB VI Metal Card | 1.4 mpd | 2 mpd |

Citi Prestige Citi Prestige | 1.3 mpd | 2 mpd |

Maybank VI Maybank VI | 1.2 mpd | 2 mpd |

AMEX Plat. Reserve AMEX Plat. Reserve | 0.69 mpd | 0.69 mpd |

| *Min. S$2,000 spend per statement month, otherwise 1 mpd for both SGD and FCY ^Min S$50,000 spend in the previous membership year, otherwise 1 mpd (SGD) and 2 mpd (FCY) | ||

All foreign currency transactions are subject to a 3.25% fee, so using your DBS Vantage Card overseas represents buying miles at 1.48 cents each (3.25%/2.2 mpd).

The DBS Vantage allows cardholders to switch between earning DBS Points or cashback, but I’m ignoring the latter because it values your miles at an awful 1 cent each. Seriously, there’s no need to ever dabble in that.

Expedia

|

| DBS x Expedia |

From 1 October 2022 to 31 March 2023, DBS Vantage Cardholders will earn 6 mpd on the first S$5,000 per calendar month spent on participating flights or hotel bookings via Expedia.

This is broken down into:

- The usual 1.5 mpd for local spending

- A bonus 4.5 mpd for Expedia transactions

1.5 mpd will be credited initially, with the 4.5 mpd bonus component credited within 45 days after the end of each spend period, defined as:

- 1 October to 31 December 2022

- 1 January to 31 March 2023

Bookings must be made through a dedicated Expedia microsite, and here’s where comparison shopping is essential- these landing pages sometimes result in higher prices than searching through public channels, so make sure you aren’t paying over the odds.

Eligible hotel bookings are those where customers make payment to Expedia at the time of booking (i.e. not applicable you choose to pay later at the hotel).

Eligible airline bookings are those made with the following carriers.

| ✈️ Participating Airlines | |

|

|

Singapore Airlines is a notable absentee, but Korean Air, Qatar Airways and Turkish Airlines could prove useful, depending on where you’re going.

Bonus miles will be awarded within 45 days after the end of each spend period, defined as:

- 1 October to 31 December 2022

- 1 January to 31 March 2023

When are DBS Points credited?

DBS Points will be credited when your transaction posts, which generally takes 1-3 working days.

How are DBS Points calculated?

Some people get concerned when they read in the T&Cs that DBS Points are awarded in S$5 blocks. That’s understandable, given how OCBC and UOB’s S$5 earning blocks result in lost miles from rounding, especially for small transactions (spend S$4.99? No points for you!).

The good news is that DBS’s calculations aren’t nearly as punitive. Here’s how you can work out the DBS Points earned on your DBS Vantage Card.

| Local Spend | Divide transaction by 5 and multiply by 3.75. Round down to the nearest whole number |

| FCY Spend | Divide transaction by 5 and multiply by 5.5. Round down to the nearest whole number |

Notice how the transaction is not rounded down to the nearest S$5; instead, it’s divided by 5 straight away. This means the minimum spend to earn points is:

- S$1.34, if spending in SGD

- S$0.91, if spending in FCY

If you’re an excel geek, here’s the formulas you need to calculate:

| Local Spend | =ROUNDDOWN ((X/5)*3.75,0) |

| FCY Spend | =ROUNDDOWN ((X/5)*5.5,0) |

| Where X= Amount Spent | |

For the full list of formulas that banks use to calculate credit card points, do refer to these articles:

What transactions aren’t eligible for DBS Points?

A full list of transactions that do not earn DBS Points can be found in the T&C.

I’ve highlighted a few noteworthy categories below:

- Amaze transactions

- Charitable donations

- Education

- Government institutions and services (court cases, fines, bail and bonds, tax payment, postal services, parking lots and garages)

- Hospitals

- Insurance

- Top-ups of prepaid accounts e.g. GrabPay and YouTrip

- Utilities bills

For avoidance of doubt, CardUp and RentHero transactions are eligible to earn DBS Points.

What do I need to know about DBS Points?

| ❌ Expiry | ↔️ Pooling | ✈️ Transfer Fee |

| 3 years | Yes | S$27 per conversion |

| ⬆️ Min. Transfer | ✈️ No. of Partners | ⏱️ Transfer Time |

| 5,000 DBS Points (10,000 miles) | 4 | 1-3 working days (for KF) |

Expiry

DBS Points expiry can be a confusing matter, because different cards apply different policies. DBS Points earned on the DBS Vantage Card expire in 3 years.

This is rather disappointing, since DBS Points earned on the entry-level DBS Altitude Card never expire. All the same, I personally don’t consider non-expiring points to be that big a factor in deciding whether or not I get a card.

Pooling

DBS Points pool across cards for the purposes of redemption. If you have 10,000 DBS Points on the DBS Vantage Card and 5,000 DBS Points on the DBS Woman’s World Card, you can redeem 15,000 DBS Points at one shot and pay a single conversion fee.

However, DBS Points are not pooled when it comes to card cancellations. If I have a DBS Vantage Card and DBS Woman’s World Card and decide to cancel the former, I’ll need to transfer my points out before cancelling or forfeit them.

Partners and Transfer Fee

DBS partners with the following frequent flyer programmes, and a minimum conversion block of 5,000 points is required (let’s ignore AirAsia, because converting points there is like throwing them away):

| Frequent Flyer Programme | Conversion Ratio (DBS Points: Miles) |

| 5,000: 10,000 | |

| 5,000: 10,000 | |

| 5,000: 10,000 | |

| 500: 1,500 |

Transfers cost S$27 per programme, regardless of how many points are transferred.

Do note that the DBS Vantage, surprisingly, is not eligible for DBS’s “auto conversion programme” (I initially thought it was an oversight, but DBS’s comms team has told me that’s how it should be).

The auto conversion programme, for the uninitiated, charges a flat fee of S$43.20 per membership year, and automatically converts DBS Points to KrisFlyer miles each calendar quarter in blocks of 500 points. It is currently available to DBS Insignia, DBS Black Treasures Elite, and DBS Altitude cardholders.

Transfer Times

DBS tells customers to expect points to be credited in 1-2 weeks, but in reality it usually takes about 1-3 working days at the very most (at least for KrisFlyer, transfer times to other programmes can be longer)

If you need your points credited instantly, you can do so via Kris+. 100 DBS Points can be transferred to 170 KrisPay miles, which can then be transferred to KrisFlyer miles at a 1:1 ratio.

| S$5 for new Kris+ Users |

| Get S$5 (in the form of 750 KrisPay miles) when you sign-up with code W644363 and make your first transaction |

Transfers are immediate, but those 100 DBS Points would normally have earned you 200 KrisFlyer miles, so you effectively take a 15% haircut.

Therefore I wouldn’t recommend taking this option, unless you need a small top-up to redeem a flight, or have an orphan DBS Points balance (<5,000 points).

Other card perks

10 free lounge visits

|

| Registration |

DBS Vantage Card cardholders are entitled to 10 free lounge visits per membership year, via Priority Pass. These lounge visits can be shared with guests; for example, the cardholder could bring his wife and two children and use four visits at one go.

Only the principal cardholder is entitled to this benefit. Once free visits are exhausted, you’ll be charged US$32 per additional visit.

10 passes may be more than sufficient for the casual traveller who doesn’t have kids, but everyone else may want to consider a $120K card that has unlimited lounge access.

| Card | Lounge Network | Free Visits (Per Year) | |

| Main | Supp. | ||

| HSBC VI | LoungeKey | ∞ | ∞ |

| Citi Prestige | Priority Pass | ∞ + 1 guest | N/A |

| OCBC VOYAGE | Plaza Premium | ∞ | ∞ |

| Maybank VI | Priority Pass | ∞ | N/A |

| DBS Vantage | Priority Pass | 10 | N/A |

| SCB VI | Priority Pass | 6 | N/A |

| UOB VI Metal Card | Dragon Pass | 4 | N/A |

| AMEX Plat. Reserve | N/A | N/A | N/A |

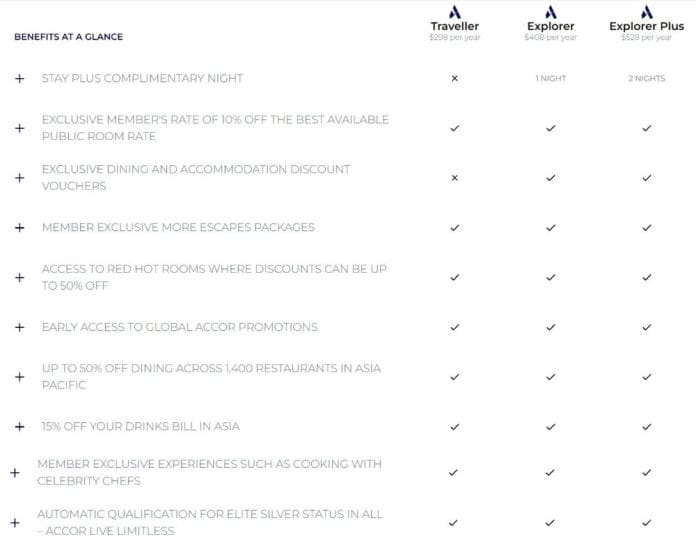

Accor Plus

|

| Registration |

DBS Vantage Card cardholders receive a complimentary Accor Plus Explorer membership with one complimentary hotel night each year. This membership will be automatically renewed each year you retain the card.

This normally retails for S$418, and includes benefits such as:

- Up to 50% off dining at participating Accor hotels across Asia Pacific

- 15% off drinks bill in Asia

- 10% off the best available public rate

- Access to Red Hot Room sales with up to 50% off

- Accor Live Limitless Silver status

The full list of benefits can be found below.

The free hotel night can be redeemed at participating Accor properties across the Asia Pacific region, including the Sofitel Singapore Sentosa Resort & Spa, Mondarin Seoul Itaewon, and Sofitel Darling Harbour Sydney. Sadly, Raffles Hotel is excluded!

DiningCity

|

| DiningCity |

DBS Vantage cardholders can enjoy “members-only discounts at over 80 of Singapore’s finest dining establishments”, through a partnership with DiningCity.

Discounts range from 15-50% off, though most of them are around the 15% mark. What’s more, the two restaurants which offering 50% off (Cali at Ascott Raffles Place and Park Avenue Rochester) can also be booked at 50% off through eatigo- no expensive credit card required.

Summary Review: DBS Vantage Card

| |||

| Apply |

The DBS Vantage Card offers the highest earn rate of any $120K card (assuming we’re looking at it from a no minimum spend perspective; otherwise that title goes to the SCB Visa Infinite), and its 60,000 miles sign-up bonus is particularly attractive for new-to-bank customers.

The 25,000 renewal miles and an Accor Plus Explorer membership with up to 50% off dining and one free hotel night can help recoup a good chunk of the S$594 annual fee too, provided you redeem that night judiciously- no ibis hotels, please.

Key misses are the lack of airport limo transfers, complimentary travel insurance, or unlimited lounge access. DiningCity discounts also look underwhelming, and certainly not a competitor to AMEX Love Dining. And it’s annoying that DBS couldn’t give evergreen points on this card, although truth be told, you should be clearing out your points every three years to avoid the inevitable devaluations.

I just feel it lacks that extra bit of oomph that would give it the leg up over competitors like the Citi Prestige or OCBC VOYAGE.

So that’s my review of the DBS Vantage Card. What do you think?

| 🦁 MileLion Verdict | |

| ☐ Take It ☑ Take It Or Leave It ☐ Leave It |

Can the Priority Pass allowances all be used in one go? Might come in handy at the PP restaurants/bars in places like SYD or MEL where a normal PP+Guest allowance ends at $72 (or zero for AmEx PP). Even handier if they did takeaway bottles…

Rule: 1 boarding pass = 1 PP swipe. the places which offer dining credit will follow this rule strictly, it’s part of the PP audit process. if you have 2 bp you can use 2 pp swipes etc.

PP T&C are not very clear when it comes to guests: they kind of say that it’s a lounge-based approach but then I could not spot the guest logo for the lounges I’ve looked up on PP website. Do you have more clarity on that, as in, 1 guest is always 1 additional swipe and, as long as I have not exhausted my credit card-sponsored PP allowance, I am good to go?

Hi Aaron

Thanks a lot for this, very helpful as always! Just to check on the below statement under “SGD/FCY Spending“, should it be “1 DBS point is worth 2 miles…” instead?

“5 DBS points are worth 2 miles, so that’s an equivalent earn rate of 1.5 mpd for local spending, and 2.2 mpd for FCY spending.”

fixed that, thanks.

Having just used the Citi Payall for my tax and also paid the annual fee, I’m struggling to see a reason to get this card as well.

That’s your problem, to me this card has little to do with annual fee/tax. So try better next time

Updated my income records (~100k) when applying for Woman’s World recently, was able to see the Vantage Card in the portal and received instant approval…so just a data point for reference.

hi aaron, do you know if the yearly renewal comes with the accor plus membership too?

the answer is in the article

Already spent all my AF budget on AMEX Plat Charge lol

Do u think it makes sense to apply for AMEX Plat Charge just for benefits (And fringe usage like card of last resort for hospitals etc, 10x accelerator purchases). And use DBS Vantage for everything else.

Not the most efficient of course but lazy to track across too many cards.

Anyone knows if DBS tax facility qualifies for the 8K? Not direct to IRAS.

Got a similar query too. The expenses exclusion applies for DBS points that’s something we all established.

But how about the $8k spending for the bonus miles. Can this be in any category?

Meaning to say, lets ignore the fact that it’s not economical miles wise to do so, but can you just spend $8k on hospital bills, don’t get the DBS points but meet the spending requirement for the bonus miles?

Hi, can I n ow of the Accor free night is only available for Asia hotel? Can I use it in Europe?

Asia is where you can find the most free hotel stays. No free night in the US just for reference. Europe might be similar too

By the way what’s the mpd of this card?

literally the first few things mentioned at the top of the article

lol

Looks like this is a close fight with OCBC Voyage. Could you please share just between Vantage vs Voyage which one is better? TIA

Vantage is better, cos DBS is sponsoring these…

Understand insurance doesnt earn miles but can it qualify for the 8k spending for bonus miles?

Got the card. Got my Accor Plus membership. It’s impossible to find any availability for the free 1 night (Accor Plus Stay Plus) anywhere. If you thought SQ Saver miles redemption is difficult, this looks like 10x more difficult. Strange why they make it so difficult as they charge 420 SGD for this.

agree, and actually can get a free room lower than $100, price above this either it is not available or you need to compensate

Is the VTMILES code still applicable if I’ve submitted the income update earlier?

Think I have found the answer in TnC on 8 July 2022 10am. Weird that bank doesn’t proceed my income update request but adjusted based on my credit limit review request. I updated my income to apply for the DBS Vantage Card. However, I have missed the Up to 80,000 Miles Sign-Up Promotion. Do I have to call in for an extension? The promotion will be automatically extended to you if you have updated your income between 23 June to 27 June 2022 to apply for the DBS Vantage Card. You need not contact us to register. This promotion extension… Read more »

I applied under the original offer for 80k miles which stated I had to be approved by July 11th. I was only approved today. Do you know if I’m still eligible?

Can confirm that it is shown on ibanking for 100k-ish annual income as well. Instant approval.

Understand Cardup (non rent) is being confirmed with DBS whether it will be considered as part of the 8k spending. What about rent via Cardup? Also ipaymy.com?

Hi Aaron, Since DBS Altitude has a auto conversion annual programme for flat fee and since vantage card points pools, does it mean the miles we earn on vantage card will auto convert to KF if we are on the Altitude auto conversion programme?

Will miles be accumulated if I use the DBS Vantage Card to make a payment through the Kris+ app? I see that only Amaze transactions have been excluded?

I’ve made some payments with Kris+ and they earned DBS points.

So just want to check, for the promo on the spending of 8K in 60 days part, does it to have to be the type that qualifies for points? Or can I literally just charge to my grabwallet and transfer back?

Could I check if you have the exclusions for the signup bonus before 1 Oct?

I met the criteria in Aug, and the customer services said it takes 120-150 days for miles to be credited. This is part of the terms and conditions. Just wondering, did anyone receive the Vanmiles reward miles or is everyone still waiting?

Same question as Gina, anyone received their miles yet?

Any idea if they are still going to give 4mpd on dining and petrol in 2023?

We will find out tomorrow!

It’s been removed from website.. Sad

Sad; Won’t be using the card much now.

Hi All,

I had spoken to DBS CSO, and it seems that Cardup payments are excluded from the $8K minimum spend in the first 2 months.

I thought this was mentioned before that Cardup was included and i also cant find any exclusion in the terms as well.

Is anyone facing the same issue or gotten your Cardup transactions included as part of the minimum spend?

Thanks.

cardup payments for rent are included in min spend, per my discussions with dbs. other cardup is not included for sign up bonus spend, but will still earn regular points

Thanks Aaron for the clarification.

Jumping on this thread to clarify, if Government institutions and services (court cases, fines, bail and bonds, tax payment, postal services, parking lots and garages) are not eligible for DBS Points does paying our IRAS Income Tax with the DBS Vantage card thru Cardup make any difference, ie earn 1.5mpd on our income tax payments?

you will earn 1.5 mpd on tax payments via cardup

Can this be used to earn 1.5mpd with simplygo?